Equity release awareness and misconceptions

Part of the Life Well Spent Report 2024

Equity release can make life-changing spends possible, such as dream holidays, renovations, gifts to family, or paying off debts. But many people don’t know the ins and outs of equity release today.

What is equity release?

Equity release is a way to get tax-free cash from the value that’s tied up in your house. The most common type of equity release, a lifetime mortgage, is a loan that’s secured against your home. This is repaid when you die or move into permanent care.

Releasing equity could enable you to take that dream holiday or give your loved ones an early inheritance – plus much more.

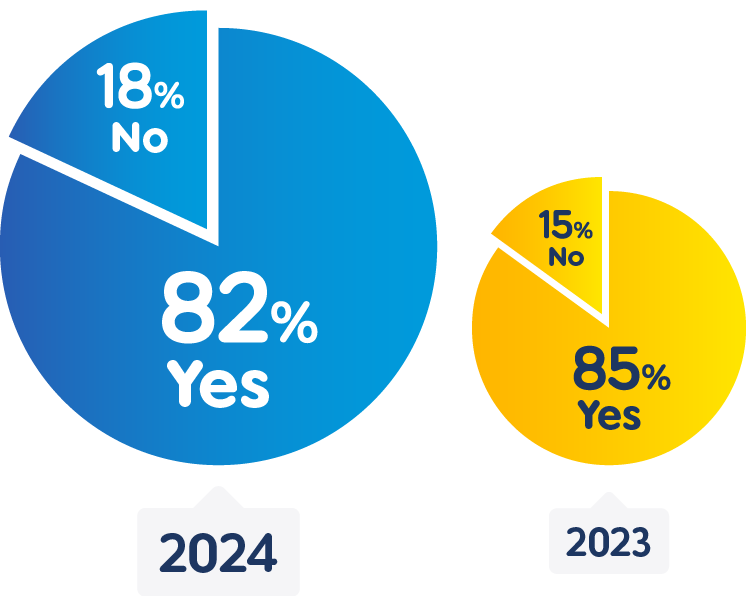

Are the over 50s aware of equity release?

When asked if they are aware of what equity release is, 82% of people over 50 say yes – 3% less than last year. And awareness rises to 91% among retirees, but this is still 4% less than in 2023.

6% of eligible* homeowners have taken out equity release – up 2% since last year – representing 3% of all people over 50. But of those who haven’t release equity, only 12% would consider it (-4%).

*Homeowners aged 55+ who are aware of equity release.

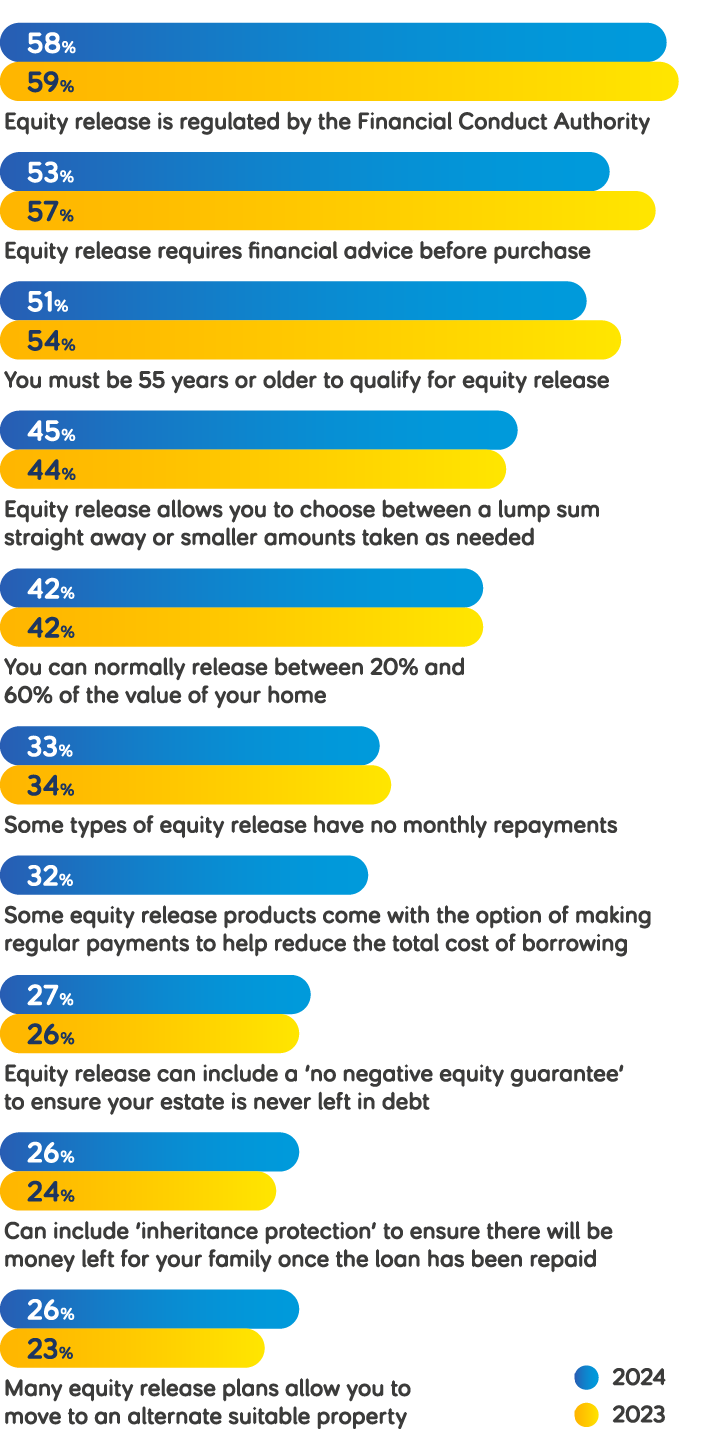

Only 6% know all the facts about equity release

Despite most over 50s being aware of equity release, many are unaware of the ins and outs. And awareness of many features has gone down since 2023.

For example, 53% of over 50s know you need expert financial advice to release equity – down from 57% last year.

And only 6% (+2%) of homeowners who haven’t released equity know all the facts about equity release.

Which of the following facts about equity release are you aware of?

The data is as follows:

- Equity release is regulated by the Financial Conduct Authority. 58% 2024. 59% 2023.

- Equity release requires financial advice before purchase. 53% 2024. 57% 2023.

- You must be 55 years or older to qualify for equity release. 51% 2024. 54% 2023.

- Equity release allows you to choose between a lump sum straight away or smaller amounts taken as needed. 45% 2024. 44% 2023.

- You can normally release between 20% and 60% of the value of your home. 42% 2024 and 2023.

- Some types of equity release have no monthly repayments. 33% 2024. 34% 2023.

- Some equity release products come with the option of making regular payments to help reduce the total cost of borrowing. 32% 2024.

- Equity release can include a 'no negative equity guarantee' to ensure your estate is never left in debt. 27% 2024. 26% 2023.

- Can include 'inheritance protection' to ensure there will be money left for your family once the loan has been repaid. 26% 2024. 24% 2023.

- Many equity release plans allow you to move to an alternate suitable property. 26% 2024. 23% 2023.

The least known fact is that equity release plans can include a ‘no-negative-equity’ guarantee, which means you’ll never owe more than your home is worth. 42% of homeowners who are aware of equity release say they didn’t know this.

A big concern for those who say they wouldn’t consider equity release is the worry that they may leave their loved ones in debt. So this unawareness could be acting as an unnecessary barrier to many people.

When the over 50s who wouldn’t consider equity release were asked why not, misconceptions once again played a part – just like in 2023 and 2022. For example, some people thought releasing equity would involve too much risk, leave their family in debt, or that they would have to pay back interest.

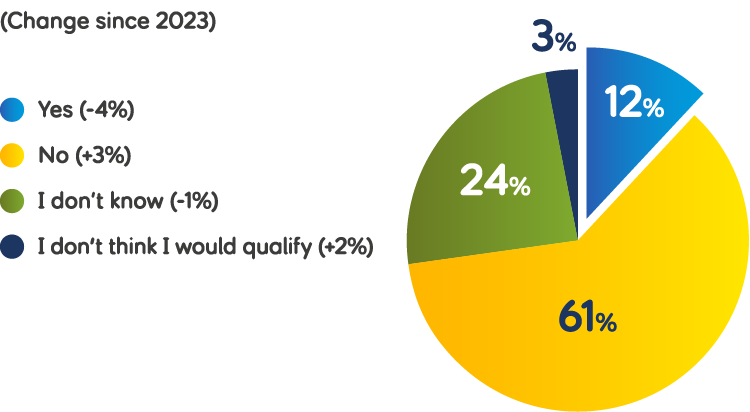

Would you consider equity release?

The data is as follows:

- Yes 12%. (-4% change since 2023).

- No 61%. (+3% change since 2023).

- I don't know 24%. (-1% change since 2023).

- I don't think I would qualify 3%. (+2% change since 2023).

However, equity release products that follow Equity Release Council standards have a ’no negative equity’ guarantee. This means someone releasing equity will never owe more than their home is worth, so their loved ones can’t be left in debt from equity release.

But it’s worth keeping in mind that all types of equity release products will reduce the value of an estate and could affect eligibility for means-tested benefits. Anybody considering equity release should discuss their options with an expert adviser.

How much equity would people like to release?

On average, people who would consider equity release in 2024 would choose to release £88,747 in total – £18,000 less than last year.

But if we look at the figures across the last three years, people would choose to release an average of £95,382.

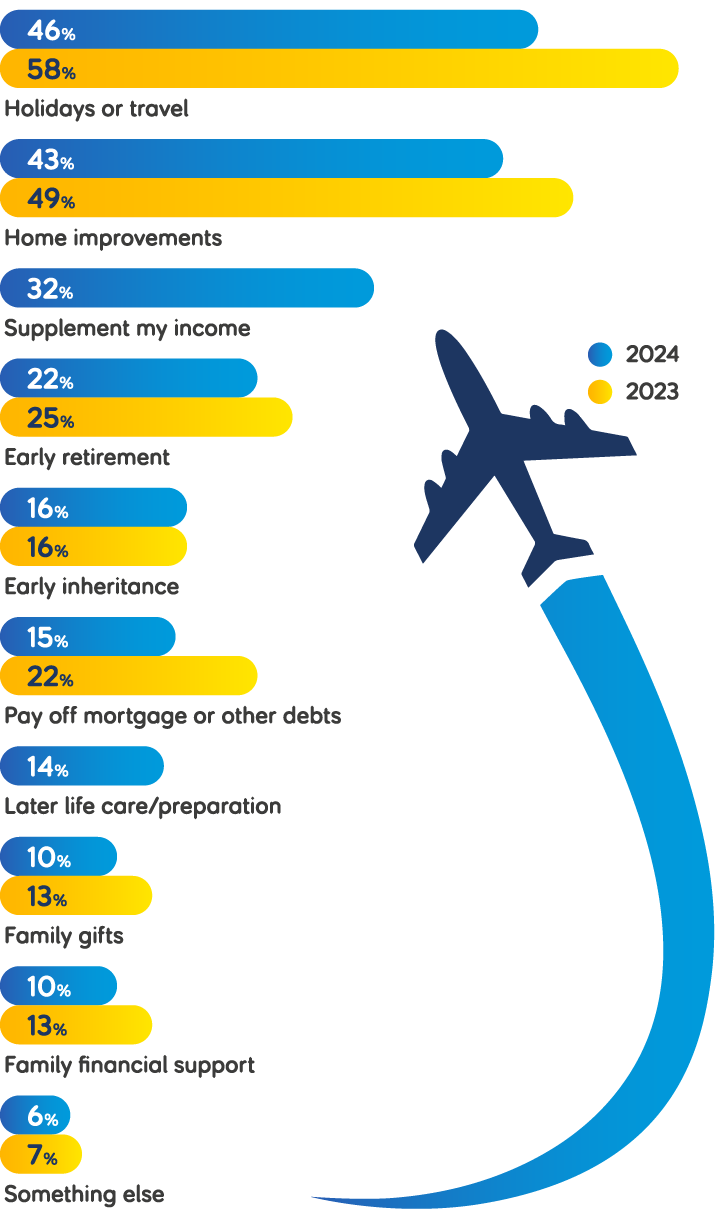

This year, 46%, would spend at least some of the cash on holidays or travel, although this is down 12% since 2023. 43% (-6%) would spend it on home improvements, increasing to 47% of women. 32% would use it to supplement their income (a new addition to this year’s survey). And 22% (-3%) would take an early retirement.

If you took out equity release, what would you spend it on?

The data is as follows:

- Holidays or travel. 46% 2024. 58% 2023.

- Home improvements. 43% 2024. 49% 2023.

- Supplement my income. 32% 2024

- Early retirement. 22% 2024. 25% 2023.

- Early inheritance. 16% 2024 and 2023.

- Pay off mortgage or other debts. 15% 2024. 22% 2023.

- Later life care/preparation. 14% 2024.

- Family gifts. 10% 2024. 13% 2023.

- Family financial support. 10% 2024. 13% 2023.

- Something else. 6% 2024. 7% 2023.

The amount of equity release people would spend on holidays has gone up to £23,028 in 2024 – up £5,493 on last year.

Whereas the amount people would gift to family has more than halved, from £36,277 in 2023 to £15,906 in 2024 – a drop of £20,371.

If you released equity, how much would you spend on each of these?

| 2024 | |

|---|---|

| Supplement my income | £61,808 |

| Early retirement | £58,561 |

| Later life care/preparation | £41,957 |

| Pay off mortgage** or other debts | £32,808 |

| Early inheritance | £31,457 |

| Family financial support | £31,563* |

| Home improvements | £25,568 |

| Family gifts | £15,906* |

| Holidays or travel | £23,028 |

*Low base size

**Equity release money must be used to pay off any remaining mortgage on your property first

We’ve seen a similar shift when it comes to early inheritance, with the amount they’d spend on this dropping from £51,773 in 2023 to £31,457 in 2024. That’s a drop of £20,316.

People would spend the most on supplementing their income – £61,808 – which is a new addition to this year’s survey. And in second they’d spend £58,561 on early retirement (a drop of £7,939). Third is another new addition, later life care/preparation, which they’d spend £41,957 on.

How are people spending the equity they've released?

Of those who’ve taken out equity release (3% of all respondents), the priorities and amounts spent differ greatly from those who are considering it.

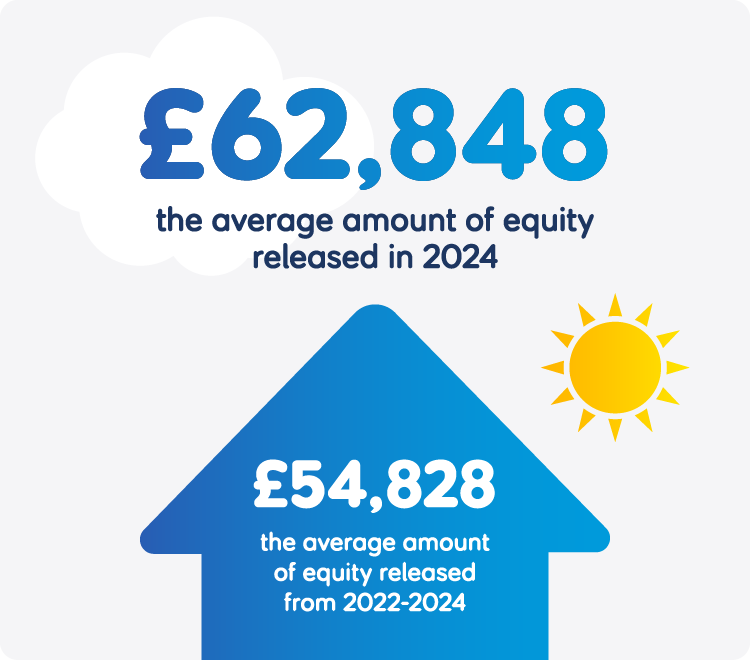

On average, they released £62,848 – £25,899 less than those in the consideration stage would like to release.

However, on average this is £11,208 more than respondents from 2023 said they had released, and £12,208 more than respondents from 2022 said they had released. And if we look at respondents from the last three years, those who have released equity say they released £54,828.

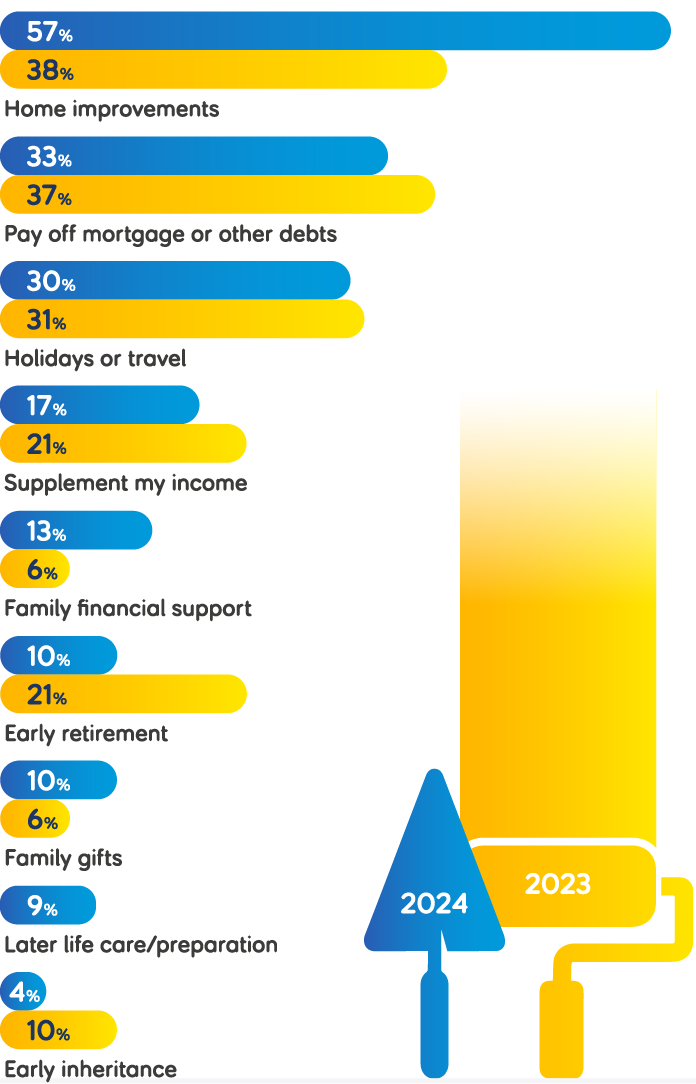

When you released equity, what did you spend it on?

The data is as follows:

- Home improvements. 57% 2024. 38% 2023.

- Pay off mortgage or other debts. 33% 2024. 37% 2023.

- Holidays or travel. 30% 2024. 31% 2023.

- Supplement my income. 17% 2024. 21% 2023.

- Family financial support. 13% 2024. 6% 2023.

- Early retirement. 10% 2024. 21% 2023.

- Family gifts. 10% 2024. 6% 2023.

- Later life care/preparation. 9% 2024.

- Early inheritance. 4% 2024. 10% 2023.

At 57%, the most popular way to spend equity release is on home improvements (+19% since 2023). Second is paying off debts (including the mortgage, which is a requirement of all equity release schemes) at 33% (-4%). And third is holidays/travel at 30% (-1%).

How much did they spend, and on what?

When we asked how much of their equity they spent on each category, ‘supplement my income’ comes out on top, with an average of £22,083.

In 2024, people who released equity spent an average of £20,913 on paying off their mortgage or other debts.

It should be noted that with only 3% of respondents taking out equity release, these findings come from a low base.

Average spend with equity release |

2024 | 3-year average (2022-2024) |

|---|---|---|

| Supplement my income | £22,083* | £19,664 |

| Pay off mortgage** or other debts | £20,913* | £26,792 |

| Family financial support (e.g. tuition fees or home deposit) | £16,444* | £15,810 |

| Early inheritance | £15,667* | £8,938 |

| Home improvements | £12,179 | £11,404 |

| Holidays or travel | £7,729* | £6,919 |

| Later life care/preparation | £6,700* | £6,700 |

| Family gifts | £5,500* | £6,352 |

| Early retirement | £4,429* | £11,434 |

*Low base size

** Equity release money must be used to pay off any remaining mortgage on your property first

They spent £6,700 on later life care and preparation, £5,500 on family gifts, £16,444 on financial support for loved ones, and £4,429 on early retirement. And they spent £15,667 on giving their loved ones an early inheritance.

And when we look at how much of their equity release they’re spending on family in total – so on financial support, gifts and inheritance – it comes to an overall average of £12,290.

Equity release and happiness

At 72% (+1% since 2023), almost three quarters of people who’ve released equity say it’s made them happier. 22% (-3% since 2023) say it’s had no impact on their happiness.

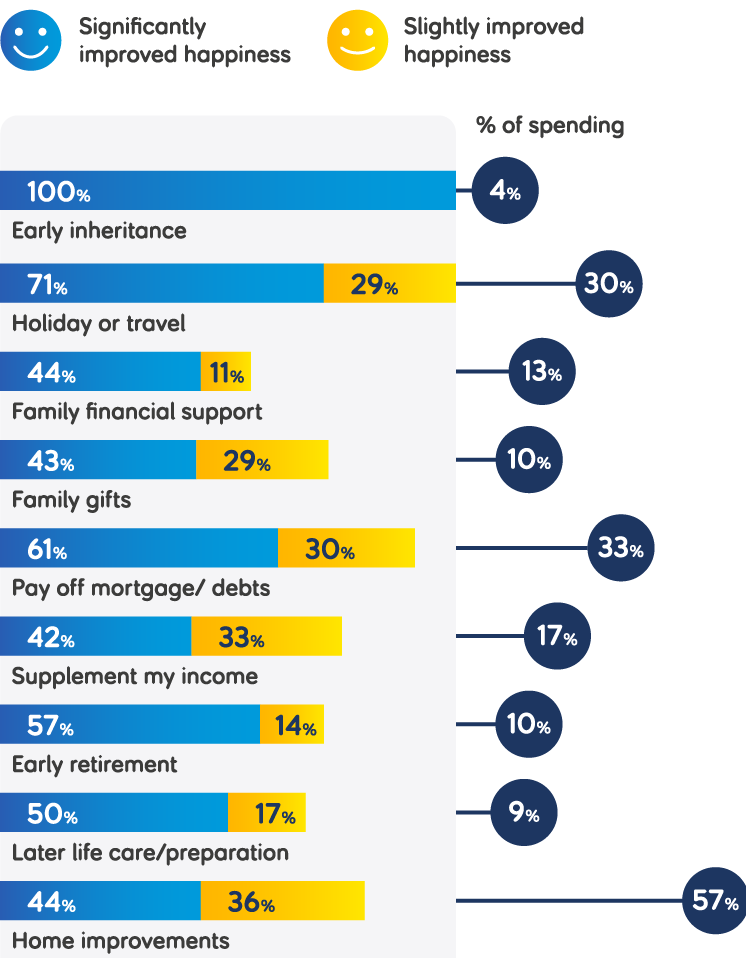

When it comes to the correlation between equity release spending and happiness, all equity release spends improved happiness for the majority of people. The spend with the least impact on happiness is family financial support (56%).

How did spending your equity release on these things affect your happiness?

The data is as follows:

- Early inheritance. 100% Significantly improved happiness. 4% of spending.

- Holidays or travel. 71% Significantly improved happiness. 29% Slightly improved happiness. 30% of spending.

- Family financial support. 44% Significantly improved happiness. 11% Slightly improved happiness. 13% of spending.

- Family gifts. 43% Significantly improved happiness. 29% Slightly improved happiness. 10% of spending.

- Pay off mortgage/debts. 61% Significantly improved happiness. 30% Slightly improved happiness. 33% of spending.

- Supplement my income. 42% Significantly improved happiness. 33% Slightly improved happiness. 17% of spending.

- Early retirement. 57% Significantly improved happiness. 14% Slightly improved happiness. 10% of spending.

- Later life care/preparation. 50% Significantly improved happiness. 17% Slightly improved happiness. 9% of spending.

- Home improvements. 44% Significantly improved happiness. 36% Slightly improved happiness. 57% of spending.

And once again, homeowners see the three main benefits of equity release as being able to continue living in your own home (39%), being able to live more comfortably (38%), and receiving a lump sum of tax-free money (36%). So if you’d like to know more, visit our equity release hub.

Reflections on equity release...

"Really pleased my son now has his own home." "I now can live on one floor and do not have to climb the stairs, and have a shower for my use." "Helped me enjoy my retirement in my dream home." "Very helpful been able to plan for the future." "It has totally freed me that I no longer am paying a mortgage." "Easy to arrange and has enabled me to retire."

Use our 60 second equity release calculator

Release tax-free cash from your home

This article forms part of our Life Well Spent report, which looks at the relationship between happiness and big purchases in later life. You can read the other sections of the report below or download the full report (PDF).